China’s display panel industry is rapidly growing, with strong upstream localization, expanding OLED adoption, and increasing demand across smartphones, automotive displays, and wearable devices.

Display panels are accelerating their integration with technologies such as 5G, artificial intelligence, and the Internet of Things, giving rise to new “Display+” business models. These innovations are empowering a wide range of scenarios, including automotive displays, smart homes, and virtual reality, continuously expanding new market opportunities.

I. Industry Chain

The display panel industry features a long and technology-intensive supply chain.

The upstream covers core materials and equipment, such as:

- Glass substrates

- Liquid crystal materials

- Polarizers

- Color filters

- Driver ICs

- Backlight modules

- Manufacturing equipment

The midstream consists of panel manufacturing and module assembly, including technology routes such as:

- LCD

- OLED

- Mini-LED

- Micro-LED

The downstream is widely applied in terminal devices such as:

- Smartphones

- TVs

- Laptops

- Tablets

- Automotive displays

- Commercial displays

- VR/AR

1")

II. Upstream Analysis

1. Glass Substrates

Glass substrates are the core foundational material for electronic display devices and semiconductor packaging. They possess characteristics such as high flatness, low thermal expansion coefficient, and high purity, which directly affect display resolution, refresh rate, contrast, and signal integrity in chip packaging.

According to the 2025–2030 China Glass Substrate Industry Market Outlook Report released by the China Business Industry Research Institute:

- In 2025, China’s glass substrate market size reached approximately RMB 36.8 billion, a year-on-year increase of 5.14%

- It is projected that in 2026, the market size will reach RMB 38.7 billion

Globally, the market is dominated by U.S. and Japanese companies:

- Corning (48% global market share)

- AGC (Asahi Glass)

- NEG (Nippon Electric Glass)

Together, they account for over 85% of the global market.

2")

In recent years, Chinese manufacturers such as Tunghsu Optoelectronic, Rainbow Group, and CSG Holding have accelerated breakthroughs. With national support and internal development, they have successfully broken foreign monopolies, achieved localization of glass substrates, and gained a significant share in the mid- to low-end market, while gradually moving toward the high-end segment.

3")

2. Polarizers

Polarizers are a core material in display panels, mainly responsible for converting scattered light into polarized light, thereby controlling whether light passes through and thereby forming contrast in displayed images.

According to the 2025–2030 China Polarizer Industry Report:

- In 2025, China’s polarizer supply reached approximately 853 million square meters

- It is projected that in 2026, supply will reach 909 million square meters

4")

In terms of company market share:

- Sumitomo Chemical holds the highest share at 22.1%

- Domestic company Shanjin Optoelectronics follows with 17.7%

- Nitto Denko: 17.5%

- Shengbo Optoelectronics: 7.1%

- Sanlipu: 3.6%

- Hengmei Optoelectronics: 3.4%

5")

3. Driver ICs

Display driver ICs are one of the main control components of display panels, often referred to as the “brain” of the panel.

According to the 2025–2030 Global and China Display Driver IC Industry Report:

- In 2025, China’s display driver IC market size reached approximately RMB 46.3 billion, a year-on-year increase of 4.04%

- It is projected that in 2026, the market size will reach RMB 47.7 billion

6")

Companies from Taiwan and South Korea dominate the global large-size display driver IC market:

- Novatek leads with a 23.9% share

- Followed by Himax, LX Semicon, and Samsung Electronics

As panel supply structures evolve, mainland Chinese companies are increasing their market share. By 2022:

- ESWIN reached 6.7%

- Chipone reached 6.3%

7")

III. Midstream Analysis

1. Global Display Panel Market Size

Driven by continuous innovation in display technology, expansion of application fields, and rapid penetration of smart terminal devices, the global display panel industry has entered a phase of rapid development.

According to the 2025–2030 Global Display Panel Market Report:

- From 2020 to 2025, the global market size grew from RMB 1.0411 trillion to RMB 1.4124 trillion

- The compound annual growth rate (CAGR) reached 6.3%

- It is projected that in 2026, the global market size will reach approximately RMB 1.4 trillion

8")

2. China Display Panel Market Size

After years of development, China has become one of the largest display panel producers in the world.

According to industry reports:

- 2023: ~RMB 660 billion

- 2024: ~RMB 690 billion

- 2025: ~RMB 720 billion

- 2026 (forecast): ~RMB 850 billion

9")

3. Display Panel Market Structure

Currently, the display panel industry is dominated by two major technologies:

- LCD: approximately 56% market share

- AMOLED: approximately 32% market share

10")

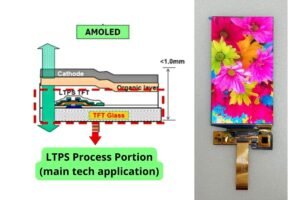

4. China OLED Panel Shipments

OLED, with advantages such as self-emission, flexibility, and high contrast, has become a key direction in display technology upgrades.

According to industry data:

- In 2025, China’s OLED panel shipment area reached approximately 5.71 million square meters, a year-on-year increase of 26.9%

- It is projected that in 2026, shipments will reach 7.6 million square meters

11")

5. OLED Market Competition

Market share distribution:

- Samsung Display: 36%

- BOE: 15%

- Visionox: 14%

- LG Display: 9%

- TCL CSOT: 9%

12")

6. Key Display Panel Companies

China’s display panel industry has formed a “dual-giant” structure led by:

- BOE

- TCL CSOT

Together, they account for over 50% of the global LCD market share.

Beyond these two leaders:

- Visionox has established a strong position in foldable AMOLED displays and is an exclusive supplier for Huawei’s foldable devices

- Tianma Microelectronics and Shentianma have captured the automotive display market, leading globally in market share and automotive certifications

13")

IV. Downstream Analysis

1. Smartphones

In recent years, driven by government consumption subsidies and supportive policies, demand in China’s smartphone market has increased.

According to industry reports:

- 2025 shipments: ~285 million units (−0.6% YoY)

- 2026 forecast: ~278 million units

14")

2. Automotive Displays

With the development of automotive electrification and intelligence, demand for automotive display panels has grown rapidly.

Applications include:

- Central control displays

- Instrument clusters

- Head-up displays (HUD)

- Rear-seat entertainment systems

Market data:

- 2023: $9.5 billion

- 2024: $10.1 billion

- 2025: $13.6 billion

- 2026 forecast: $15 billion

15")

3. Smart Wearables

According to industry reports:

- 2024 global shipments: 190 million units (−1.4% YoY)

China market:

- 2024: 61.16 million units (+19.3%)

- 2025: 73.9 million units (+20.8%)

- 2026 forecast: 75 million units

China remains one of the largest wearable device markets globally.

16")

-300x300.jpg)